COVID-19

The Coronavirus crisis has wreaked havoc on the entire country. Each of us has been directly affected in one way or another by this disease. Jobless claims are at an all time high, the economy has virtually shut down, and non-essential businesses are required to close their doors. Even though social distancing measures are in place and the stay-at-home order is active, thousands of lives have still been lost because of this deadly disease. Recently reported by NPR, the Fed is doing everything they can to keep financial markets functioning and credit available to households (Horsley, 2020). This included cutting interest rates to nearly zero. Specifically, the mortgage industry has seen many changes recently because of this. Low rates has caused a Refinance Boom. Homeowners are seeing an opportunity to refinance their current mortgages or even begin home purchases or remodels.

Low Rates, Refinance Boom

As the economy has been faced with a virtual shut-down, mortgage rates have seen record low numbers. This has created a high demand for people to refinance their current mortgages. In an article titled, “Mortgage Crisis and Fed Unintended Consequences”, Barry and Dan Habib from MBS Highway, explain how this has created a dilemma for lenders in the midst of COVID-19.

To fight the risks of borrowers who may have difficulty paying their mortgages in the event of a job loss, many lenders have created additional temporary guidelines to ensure that borrowers receiving mortgages have the ability to make their mortgage payments. Some of these borrowers may not have a lot of reserves and have higher debt-to-income ratios, which puts them into a more vulnerable position in the event of job loss. To combat this, many lenders have implemented higher credit score requirements, lower debt-to-income requirements, and even the suspension of bond and non-QM loans.

Greater Risks, Higher Volume

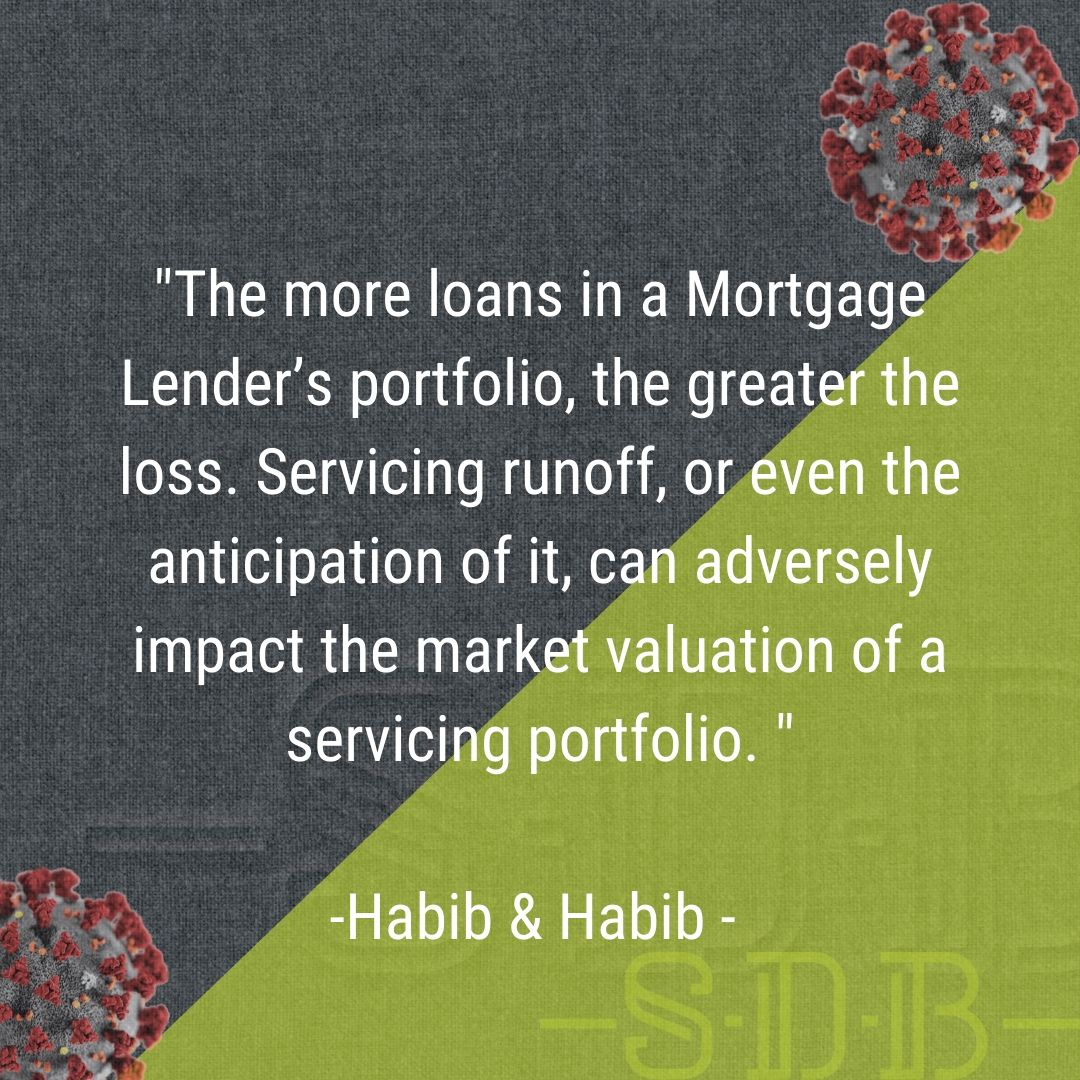

“As you can imagine, when interest rates drop dramatically, there is an increased incentive for many people to refinance their loans more rapidly. This causes the loans that a Servicer had on their books to pay off sooner…often before that 3-year breakeven period. This servicing runoff creates losses for that Mortgage Lender who is servicing the loan. The more loans in a Mortgage Lender’s portfolio, the greater the loss. Servicing runoff, or even the anticipation of it, can adversely impact the market valuation of a servicing portfolio. But at the same time, Lenders typically experience an increase in new loan activity because of the decline in interest rates. This gives them additional income to help overcome the losses in their servicing portfolio.”

Even with low rates people may not be able to pay

“But the Coronavirus has caused a virtual shutdown of the US economy, which has created an unprecedented amount of job losses. This adds a new risk to the servicer because borrowers may have difficulty paying their mortgage in a timely manner. And although the Servicer does not own the asset, they have the responsibility to make the payment to the investor, even if they have not yet received it from the borrower. Under normal circumstances, the Servicer has plenty of cushion to account for this. But an extreme level of delinquency puts the Servicer in an unmanageable position.” (Habib & Habib, 2020, para. 4-5).

The article continues to explain that a “borrower who cannot make his/her first mortgage payment causes that loan to be ineligible to be sold to an investor. This means that the Servicer must hold onto the asset itself, which ties up their available credit. And with so many new loans being originated of late, the amount of transactions that will not qualify for sale is significant. (Habib & Habib, 2020, para. 7)

Good News

Although the entire economy and mortgage industry are seeing difficulties that rival those of the great depression and 2008 recession, these difficulties are a direct result of the COVID-19 pandemic, and all should be temporary. Once things get back to normal, the entire economy should come back with strength. Restaurants and bars will be full, construction will resume in full force, real estate will be in high demand which will prompt homeowners to remodel or renovate, and mortgage rates may see record low numbers once again. The entire country is struggling with difficult times, and although some of these changes are challenging, there is a light at the end of the tunnel.

Speak to a Professional

During these uncertain times, it is important to speak to a professional who can help navigate you through the ever-changing mortgage landscape. If purchasing a home or refinancing your current mortgage interests you, now is the time to start the process. Just like the changes we have seen to the Coronavirus over the last few weeks, we have also seen changes to the mortgage industry, and we will continue to see changes in the weeks and months ahead. We have faith that the effects of this virus will be temporary, and this will return to normal in the months ahead. For the time being, please remember to take the proper precautions to keep yourself and others safe and healthy.

Written by Casey Robbins of Fairway Mortgage, Apr 8th, 2020

Habib, B., & Habib, D. (2020, March 26). Mortgage Crisis and Fed Unintended Consequences. Retrieved April 7, 2020, from https://mbshighway.com/mortgage-crisis.html

Horsely, S. (2020, Apr 6). Fed Goes All Out To Keep Economy Alive During Coronavirus Shutdown. Retrieved April 7, 2020, from https://www.npr.org/2020/04/06/826894304/fed-goes-all-out-to-keep-economy-alive-during-coronavirus-shutdown

Recent Comments